Think you've enough saved for your old age? Think again!

A few years ago, when I worked in an office, we once briefly discussed pensions. I was staggered that all of the new recruits - clever graduates in their mid twenties - had chosen not to pay into the company pension scheme; they felt they had other priorities, and that they would be able to save for a pension later in life. Anyone in that position now should read the following and perhaps consider where they might be in forty or more years time.

+ + +

This morning I was updating a spreadsheet I keep on Viv's and my pensions. I like to update it every year, tracking our finances and at least making an attempt to work out how long it is that our savings might last. It's something that I think many of us are recommended to do, especially those of us that don't get substantial final salary pensions.

To produce such a plan you need to make some assumptions about your financial needs in the future; you need to think about how your lives may change, whether both of you will live into your eighties, and what your needs will be if one of you needs paid assistance.

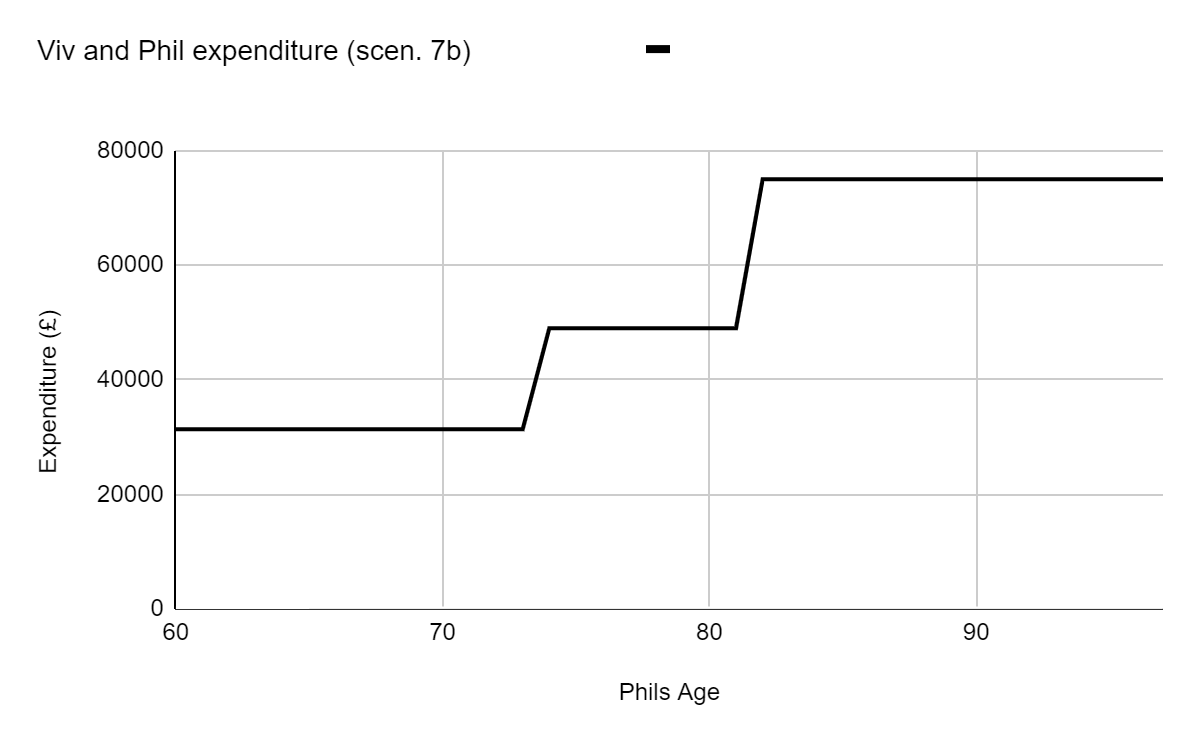

In the past I'd made some basic assumptions: one of the key ones was that our expenditure needs would not increase from current levels. That, I realised, is not a safe assumption to make: if you need help to have a bath twice a week, or, say, two carers for two hours a week, will perhaps cost you at least £60 a week. That's £3000 a year, give or take a bit. Then add on a cleaner for a few hours here and there, a gardener maybe three hours a week and your annual 'needs' in terms of income are maybe £8K higher than at present. That sort of 'care', by the way, may be felt essential, but the authorities won't necessarily pay for it. If you want it you will have to pay!

Then there is another problem: pensions are at least partly only paid to living people. When you die your state pension stops, as does your workplace pension if you have one, or it may pay half as a 'widows pension' to your partner if you're lucky and/or married. If one of you dies 'young' - under seventy, perhaps - and the other lives into their nineties, needing help around the home, the costs can be crippling, while income may almost halve: that £8K a year becomes 120K over fifteen years. That is only for a very basic level of 'care': daily visits from carers might put annual bills up over £15K or even £20K, and these might be more necessary for someone who is widowed, leaving them looking at bills perhaps pushing up to £200K or more.

So, when youngsters are working out how much they need in their pension pots, what should they be thinking? I'd suggest they need to consider

- having enough to clear their mortgage when or before they retire

- having sufficient income to keep them in a reasonable lifestyle - that's not going to be much under £20K for one person or £30K for a couple - for every year they may live in retirement, and calculate that this might be 30 years for someone retiring at 65

- having at least a further £200K buffer to cover potential care costs to help them as they get older and become more vulnerable

- subtract from this what they are guaranteed to get from the state pension

+ + +

The traditional view of 'care' is of old folks in a care home. The costs for this is astronomical - a grand a week upwards for those who pay for it; councils pay much less, so those whose funds are exhausted are, in effect, subsidised by others, thereby accelerating the speed at which their funds will be exhausted.

Some statistics suggest that the average 'service user' is in a care home for 26 months; or a tad over two years. The going rate for that, then, is perhaps 110 grand. Therefore, you should perhaps add that into the amount you think you need to have in order to retire.

Further, anyone on a 'generous' final salary pension should make a point of salting away some money as it comes in, for it may not increase enough over time to pay care costs.

+ + +

If you need care, and the local authority agrees this, they may assist you with benefits - attendance allowance, for example, which can be up to £150 a week dependent upon needs if you stay in your own home - and they may also be prepared to arrange your care for you. They'll bill you (or your estate) for this in the long term, you're only entitled to 'free' care if you have as little as £14K savings.

Staying in your home is, arguably, good for your family if you are able to do it, and avoid moving into care, because you or your family will not be required to sell your home to pay for care if you remain resident in it. However, there might not be as much state assistance available to pay for in-home care as there is to pay for residential support.

+ + +

Yes, it's a mess.

The government has been saying they want to do something about this mess'. The spectacle of old folks having to sell their homes to pay for care is, it seems, troubling. But why? Is it that we have all been led to think that our homes are sacrosanct, that we will be able to pass them on to our children?

Shouldn't we be using our assets to pay for our care, rather than relying on the state? The Cameron regime proposed a ceiling of, I think £50K, for the amount that anyone would have to pay for their own care. How would care beyond that be funded? Who would decide what constitutes 'care' and what doesn't - cleaning the home, is that care? A bath once a day, or just once a week? We'd end up with a ministry of mandarins reviewing every claim and splitting hairs over whether it was necessary to have a carer help someone to go shopping. You already get this sort of thing with regards to incontinence pads: the state provides three a day for genuinely incontinent people. Those that only get what the state decides is appropriate spend much of their day sat in their own urine and faeces. Is that really the sort of world we want for our old folks - including us, in years to come?

No, the younger generation should let them spend their money, including the capital in their homes, on their own care, if that is their wish. If youngsters are worried about their potential inheritances they could offer to provide some of that care; if they are not prepared to do that, might it be a good idea for them to look at where their money is going?

Comments

Post a Comment